![]()

4 strategies for coping with market volatility

Emotions often play a role in decision-making. When it comes to considering investment decisions in a volatile market, however, following your emotions too closely may point your investments in the wrong direction.

Many factors can inform investment decisions: Financial goals, asset allocation and diversification strategies, tax benefits and indirectly, how investors feel about the market. It’s this last factor that you can control most closely.

Common investor emotions: Euphoria vs. despondency

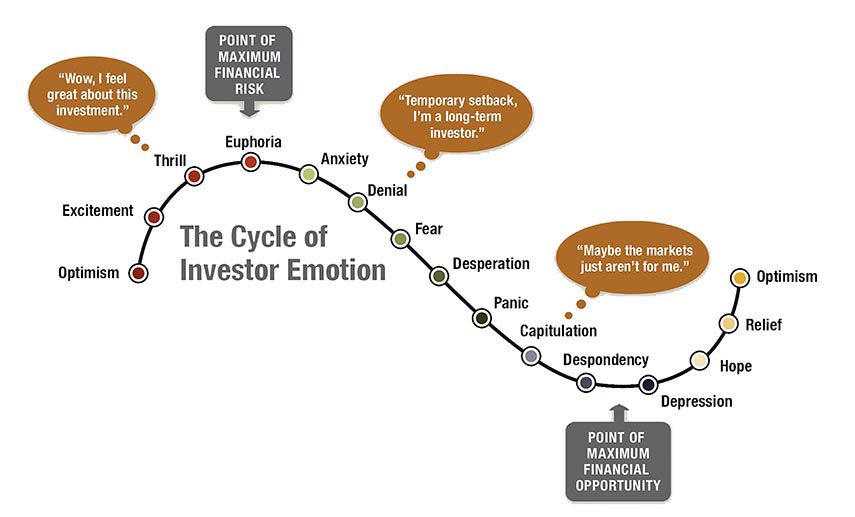

When a market is in an upswing, investors sometimes believe it has nowhere to go but up. They may even start to feel euphoric, and that euphoria can lead to making investments in overheated markets. However good the feeling, though, those might be better times to hold or sell.

“We certainly saw that just before the financial crisis in 2007,” says Rob Haworth, senior investment strategist for U.S. Bank. “In the housing market, houses would turn over within weeks because people believed in the inevitability of housing price gains and perhaps magnificent housing price gains.”

That euphoric feeling is at one end of the emotional spectrum for investors, based on a common cycle of investor emotions. At the other end is despondency, which can cause investors to foresee only further declines in the market and pull back — or even exit markets — not realizing that it could be an opportune time to buy.

“The most dramatic example of this was in the depths of the global financial crisis as investors fled stocks at the end of 2008 and in early 2009,” says Haworth. “Despite recovery later that year, investors generally didn’t return until late 2010, losing out on significant gains from the market recovery.”

Source: U.S. Bank

Common investor behavior during market uncertainty

There are generally three different stages of investor behavior that can occur with market uncertainty. All investors won’t go through each stage, but they represent common emotions people have and resulting actions they may take.

- Reactionary

- Some investors feel the need to take immediate action at the first sign of market uncertainty, either buying or selling without engaging in deep analysis.

- Their time horizon, investment style or patience level may be short, and their reaction time follows that.

- Some investors may get stuck in this phase if they’re feeling a high level of anxiety or reacting to ever-changing information.

- Liquidity

- This stage is distinct from the reactionary stage in that certain investors are forced to sell assets.

- In this kind of environment, volatile prices may trip margin and risk boundaries, selling can trigger more selling.

- Fundamental

- This stage is shaped by investors who are not driven to make buy or sell decisions unless extreme price swings emerge.

- Investors sacrifice speed for analysis, waiting to make investment decisions based on the longer-term implications of a given event.

The beginning of the COVID-19 pandemic in 2020 is an illustrative example of investor reactions that followed the three-stage sequencing. Increasing evidence of negative economic impacts on global trade from China’s shutdown to combat the virus pressured equity markets in late February.

By mid-March, stocks had declined more than 20% leading to the liquidity phase as losses forced some investors into sales to meet obligations. The market reached its low on March 23; the Federal Reserve intervened and transitioned investors into the fundamental stage.

4 strategies for navigating market volatility

Market volatility depends on many factors, and it will never disappear. It’s essential for investors to understand how to manage their emotions in the face of volatility. Four steps are key.

- Stick to your plan

- Review your financial plan and determine if you’re still comfortable with it. If you don’t have one, take the time to establish one.

- Base decisions on your long-term goals and ignore daily market fluctuations. Are you saving for retirement? A large purchase? Your child’s education? That goal will determine your asset allocation strategy and time horizon.

- Your financial plan and investment strategy should account for normal market volatility, so turn off the news and focus on the long term. Be sure to check in on the progress in your portfolio at least annually and review your plan whenever you have a major change in your life.

- Examine your personal tolerance for risk

- While no one likes seeing prices move against them, if the current market downturn is particularly difficult to stomach, talk with your financial professional.

- You may determine a more conservative investment mix can alleviate your anxiety while still pursuing your financial goals.

- Diversify your holdings

- To reduce risk and account for volatile markets, your portfolio should include investments that have higher returns in different scenarios. For example, industrial stocks may do well when the economy is booming but not during a downturn. On the other hand, consumer-staples companies that sell everyday goods such as toiletries and food can offer better returns through a recession.

- Fixed-income investments, such as bonds, generally can provide the potential for steadier returns than stocks. Read more about lower-risk bonds that can help diversify your portfolio.

- Expect — and accept — volatility

- To reduce the impact of emotions on your investment decisions, consider how similar economic cycles have unfolded in the past, both in the U.S. and international markets.

- Rather than attempting to time the market, focus on time in the market. While past performance is not a guarantee of future results, investors with diversified portfolios who stay in the market have historically and consistently experienced steady gains over time.

Bonus strategy: Take some of the guesswork out of investing

Whether you work with a financial professional or invest through a robo-advisor, we’re here to help you balance your risk.

- A wealth management professional from U.S. Bank or U.S. Bancorp Investments can offer an objective perspective and help you manage through uncertain market conditions.

- A robo-advisor, such as Automated Investor from U.S. Bancorp Investments, selects, monitors and rebalances your investment portfolio as needed to help keep your financial goals on track, even when markets are volatile.

Learn more about investing options from U.S. Bancorp Investments.

Learn more

Related content